Magnificent Seven: More diverse than they may appear

The Magnificent Seven are more diverse businesses than their shared label suggests

.

The “Magnificent Seven.” It’s an understandable, memorable, and concise term, but its simplicity masks important distinctions. With the backdrop of strong U.S. stock market performance attributed to a handful of technology companies, the group’s run has fuelled questions about market concentration. When we look more closely, we see a clutch of U.S. stock market leaders that are more diversified than some may think.

The Magnificent Seven goes well beyond AI

Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla offer a wide range of products and services, with some areas of overlap. Certainly, their activities extend well beyond AI. The companies have a diverse footprint across industries, variously functioning as global marketplaces, cloud computing providers, and even automobile manufacturers and physical grocery store operators.

The Magnificent Seven business models span how we work, play, and consume

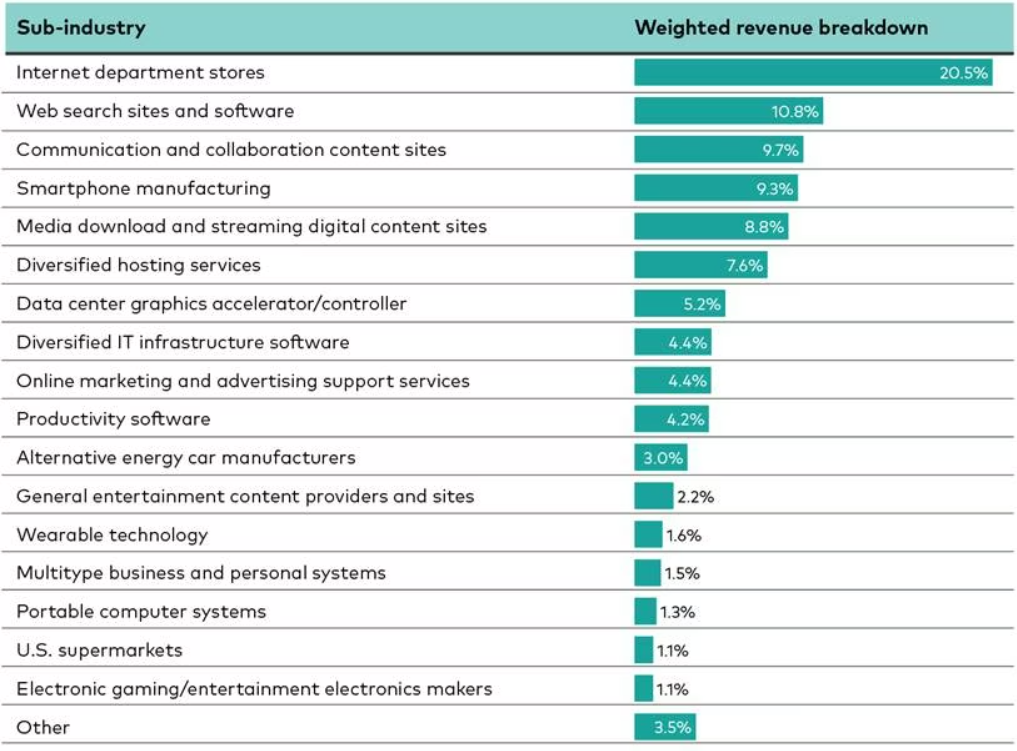

Sources of the companies' combined 2025 revenues of $2.2 trillion

Notes: Weighted revenue breakdown is the proportion of combined revenues attributed to a given source. It is determined by aggregating the revenue from each source across companies and then dividing this figure by the total revenue from all companies combined. Revenues are based on the company’s reported annual fiscal year total revenue for 2025. Sum may not total 100% due to rounding.

Sources: Vanguard calculations, based on data from FactSet, as of January 2026.

Consider a few examples:

- Amazon: Nearly two-thirds of its revenue comes from digital mall operations, approximately one-quarter from cloud services, and the remainder from online marketing and advertising services.

- Apple: Half its revenue comes from smartphone sales, one-quarter from media downloads and content streaming, and one-quarter from a mix of computer hardware, cloud storage, and wearable consumer electronics.

- Microsoft: Forty percent of its revenue comes from end-user home and office software, approximately one-third from back-end office infrastructure software, and the remainder from a mix of internet and data services, electronic gaming, and enterprise technology consulting.

While all three companies serve both consumers and commercial clients, their revenue exposures vary meaningfully across and within each company.

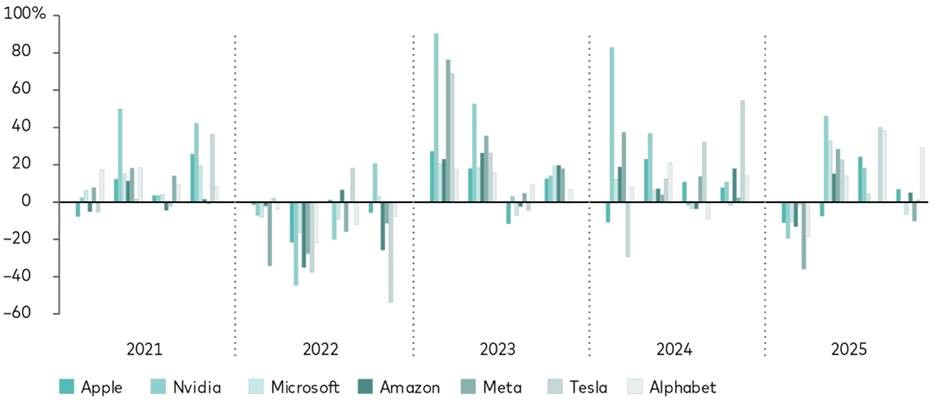

“The diverse revenue sources matter because they show that the Magnificent Seven’s business models span different end-users and markets,” said Erich Pingel, an analyst in Vanguard Investment Strategy Group. “Differences in business models also mean differences in risk-factor exposures, which helps explain why their stock prices do not move entirely in lockstep.”

The Magnificent Seven stocks have not moved in lockstep

Quarterly total returns of common stocks, Q4 2020-Q4 2025

Sources: Vanguard calculations, based on data from FactSet, as of December 31, 2025.

Seven stocks: Neither narrow nor self-contained

“The Magnificent Seven currently represents around 30% of the U.S. stock market. The companies are often portrayed as a monolith, but their business models tell a different story,” said Rodney Comegys, chief investment officer, Vanguard Capital Management, and head of Global Equity. “Their commercial and equity market success coexists with meaningful differentiation at the company level—making it unlikely that all of them will disappear or experience significant drawdowns at the same time. They share a label, not a business model.”

For investors with long time horizons, it’s worth considering how creative destruction—the process by which innovation disrupts products, technologies, and companies—recasts market leadership.

Comegys said that those inclined to consider the market’s evolution over short periods should recognize that market leadership often changes—and that the human tendency to expect trends to persist is just one factor that makes it hard to predict who the new winners or laggards will be or when the transition happens.

The world is more interconnected and interdependent than ever, due in no small part to technological progress. Although the Magnificent Seven share common elements, the companies and their stocks are not interchangeable. Their business models, strategies, and consumer bases vary—and so has the performance of their stock prices.

Vanguard

15/04/2026

vanguard.com.au

More Articles

Your 30 June superannuation checklist

Five easy ways to get more into your super fund before the end of the financial year With the end of the...

Check out what Uses the Most Internet Traffic: Data from 1994 to 2026

The evolution of global internet traffic from 1994 to 2026, tracking which technologies, platforms, and...

Minimum pension drawdown not the only thing to consider as 30 June approaches

As 30 June approaches, SMSF members drawing a pension need to think about meeting minimum drawdown obligations...

What’s your risk profile?

Understanding your risk profile is one of the most important steps you can take as an investor. It helps shape...

ASIC urges Aussies to check for unclaimed money

AISC is urging Australians to check if they have lost or unclaimed money, with approximately $2.7 billion...

PAYDAY SUPER STARTS 1 JULY 2026 – Planning guides

From 1 July 2026, super contributions will need to be paid at the same time as wages. . The current...

Six strategic investment moves for mid-career women

As women enter their mid-career years, many begin to earn more and have greater capacity to invest. Making the...

Commercial v residential: Be aware of ‘nuanced’ changes

The proposed capital gains tax changes announced in the budget are far more nuanced than the headlines...

Heathmont Financial Services Pty Ltd (ABN 68 106 250 104) trading as Heathmont Financial Services is a Corporate Authorised Representative (No. 262098) of Knox Wealth Management Pty Ltd (ABN 74 630 256 227), Australian Financial Services Licence Number (AFSL) 513763.

Julian McGoldrick is an Authorised Representative (No. 262098) of Knox Wealth Management Pty Ltd AFSL 513763.