Portfolio Construction & Diversification

By: Sofie Korac, Principal Adviser

Prudentia Financial Planning Pty Ltd

When it comes to investing, I’m sure you have heard of the saying “don’t put all your eggs in one basket!” What does this mean and how does this translate to creating a diversified portfolio?

A diversified portfolio means investing into a range of different assets and asset classes that have different performance and risk characteristics. In addition to this, the assets need to perform differently at different points in the market cycle.

The below chart shows a technical representation of the correlation between different asset classes:

Source: Lonsec

How to interpret the numbers:

+1.00 = 100% positive correlation between two assets i.e. performance of both assets move in the same direction over a period of time. For example, if the value of one asset goes up, so does the other. Likewise, if the value of one asset goes down, so does the other.

-1.00 = 100% negative correlation between two assets i.e. performance of the two assets move in the opposite direction over a period of time. For example, if the value of one asset goes up, the value of the other asset goes down, and vice versa.

0.00 = no correlation between two assets i.e. sometimes the value of the two assets move in the same direction and sometimes in opposite directions. There is no relationship between the performances of the two assets.

The closer the number is to +1, the greater the positive correlation. The closer the number is to -1, the greater the negative correlation.

Note: Correlation does not relate to actual performance. A positive correlation does not mean two investments perform the same, it just means they move in the same direction.

In a diversified portfolio, you ideally want there to be little or no correlation between the various investments used. However, in reality it can be difficult to achieve this as correlations between asset classes don’t stay static. The correlation between two assets may be neutral or negative during normal market conditions, but may become more highly correlated during a market crisis.

We saw this last year when bonds and equities both lost value over the same time period. These two asset classes normally have negative correlations. Bonds are generally used to help protect a portfolio when equities fall in value during a bear market. When there is an economic downturn, interest rates usually fall which is good for bonds and helps stimulate the economy. Last year however, we say rising inflation leading to rising interest rates and a slowing economy resulting in falling asset prices within bonds, equities and property. The perfect storm you could say.

But this year, it seems to have reversed. Both bonds and equities have made a strong recovery. Some assets have recovered better than others, while some have had a further decline in value.

You might then ask, why don’t we just invest in the best performing assets?

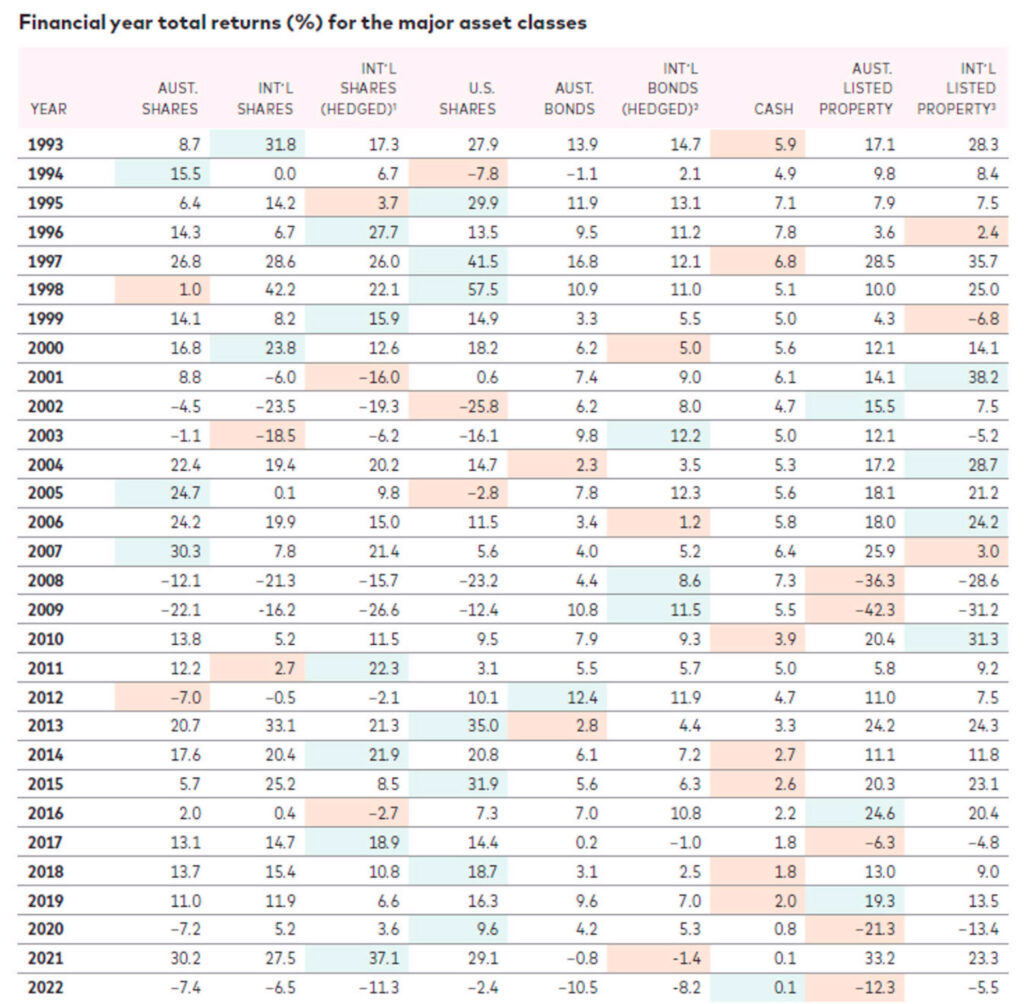

We know from experience, that past performance does not always equal future performance. The chart below shows the performance of different asset classes over the years.

Source: Vanguard

You can see on the last row that the 12 months to 30 June 2022 was an unusual year in that all asset classes fell in value including cash, if you take into account inflation.

It is almost impossible to predict future performance of an asset class consistently over time. Having a portfolio that has a broad level of diversification means we don’t have to second guess the market. Regular re-balancing between the various assets ensures you take advantage of market movements when they occur and to maintain your desired level of risk within the portfolio. Regular investing of cash also ensures your wealth continues to grow and compound over time.

Successful investing depends not on market timing or picking the winning investment, but rather on broad diversification, keeping a long-term perspective and the discipline to stay invested when things get tough.

More Articles

Your 30 June superannuation checklist

Five easy ways to get more into your super fund before the end of the financial year With the end of the...

Check out what Uses the Most Internet Traffic: Data from 1994 to 2026

The evolution of global internet traffic from 1994 to 2026, tracking which technologies, platforms, and...

Minimum pension drawdown not the only thing to consider as 30 June approaches

As 30 June approaches, SMSF members drawing a pension need to think about meeting minimum drawdown obligations...

What’s your risk profile?

Understanding your risk profile is one of the most important steps you can take as an investor. It helps shape...

ASIC urges Aussies to check for unclaimed money

AISC is urging Australians to check if they have lost or unclaimed money, with approximately $2.7 billion...

PAYDAY SUPER STARTS 1 JULY 2026 – Planning guides

From 1 July 2026, super contributions will need to be paid at the same time as wages. . The current...

Six strategic investment moves for mid-career women

As women enter their mid-career years, many begin to earn more and have greater capacity to invest. Making the...

Commercial v residential: Be aware of ‘nuanced’ changes

The proposed capital gains tax changes announced in the budget are far more nuanced than the headlines...

Heathmont Financial Services Pty Ltd (ABN 68 106 250 104) trading as Heathmont Financial Services is a Corporate Authorised Representative (No. 262098) of Knox Wealth Management Pty Ltd (ABN 74 630 256 227), Australian Financial Services Licence Number (AFSL) 513763.

Julian McGoldrick is an Authorised Representative (No. 262098) of Knox Wealth Management Pty Ltd AFSL 513763.