What it will take to close the super gap between men and women

There’s a lot of talk about in how to close the super gap between men and women, with women often retiring with far less than men.

The main drivers of this are due to women both earning less and taking time out of the workforce to care for children and other family members.

In a previous column, I discussed steps women and their partners can take to close this gap.

A new report from Women in Super and research firm Rice Warner reinforces the risks that the gender gap poses for women and offers data on the roots of the problem.

Previous research showed that because women have less in super and rely more heavily on the age pension, they are more likely than men to face financial insecurity and poverty in retirement.

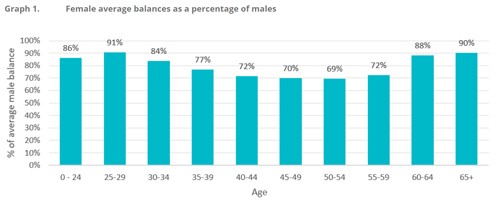

As you can see from the Rice Warner data in the chart below, the super gap starts to widen when women are in their 30s, suggesting that taking time out of the workforce to rear children diminishes income and super contributions.

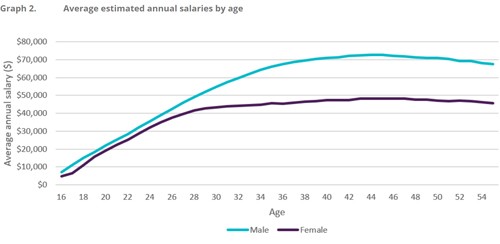

The research also demonstrates that women start out their careers with pay that is close to their male counterparts, only to see a gap emerge as women enter their 20s and 30s. The source of this divergence is not clear, but one likely cause is that women are more likely to leave work to take care of children or family members, missing out on years in the workforce when promotions and pay raises are most likely.

Investment research shows that men tend to invest more aggressively than women, but Rice Warner said this difference did not contribute significantly to the super gap.

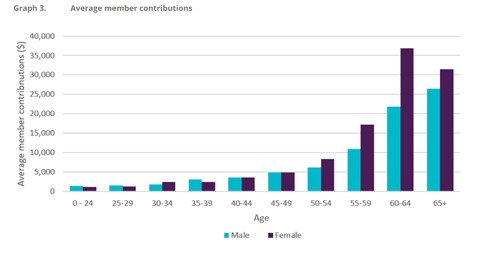

The positive news is that women are taking action to close the gap. They contribute more to super, especially as they approach retirement, which boosts their balances at a crucial stage.

Many women don’t earn enough to make extra contributions, however, and those who do likely can’t compensate enough for years of reduced earnings and super guarantee payments. The roots of the super pay gap are many — gender inequality, the challenges and costs of child care and super policy. Fixing the problem will require changes on all those fronts.

Written by Robin Bowerman

Head of Corporate Affairs at Vanguard.

21 May 2019

vanguardinvestments.com.au

More Articles

Most Reliable Car Brands in 2026

Check out which car brands are the most likely to stay on the road and not cost you a fortune to...

Super versus trusts: What is the best option with Div 296?

Super used to be clearly the “best” option due to low tax rates but the increasing complexity of things...

AI use needed with proper safeguards

The SMSF Association has suggested practitioners servicing the sector must equip themselves with more than...

Thinking of establishing an SMSF? Don’t skip reading the rules

As the establishment of new SMSFs continues to rise, the ATO is reminding potential trustees to ensure they...

Are downsizer contributions losing steam?

Tax Office data shows fewer people used its super scheme in 2024-25 . Introduced in 2018, the home...

Investment and economic outlook, February 2026

latest forecasts for investment returns and region-by-region economic outlook . Australia A rate...

Coercive control in SMSF becoming a hot issue

AFCA is anticipating there will be more focus on coercive control and elder abuse going...

What to look for when choosing a financial adviser

Here's how to find a financial adviser who can provide the right support for you . We believe...

Heathmont Financial Services Pty Ltd (ABN 68 106 250 104) trading as Heathmont Financial Services is a Corporate Authorised Representative (No. 262098) of Knox Wealth Management Pty Ltd (ABN 74 630 256 227), Australian Financial Services Licence Number (AFSL) 513763.

Julian McGoldrick is an Authorised Representative (No. 262098) of Knox Wealth Management Pty Ltd AFSL 513763.