What it will take to close the super gap between men and women

There’s a lot of talk about in how to close the super gap between men and women, with women often retiring with far less than men.

The main drivers of this are due to women both earning less and taking time out of the workforce to care for children and other family members.

In a previous column, I discussed steps women and their partners can take to close this gap.

A new report from Women in Super and research firm Rice Warner reinforces the risks that the gender gap poses for women and offers data on the roots of the problem.

Previous research showed that because women have less in super and rely more heavily on the age pension, they are more likely than men to face financial insecurity and poverty in retirement.

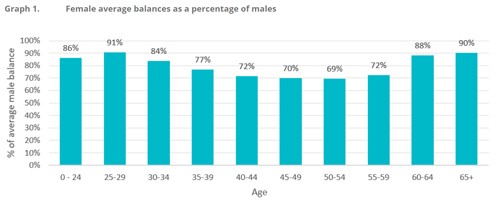

As you can see from the Rice Warner data in the chart below, the super gap starts to widen when women are in their 30s, suggesting that taking time out of the workforce to rear children diminishes income and super contributions.

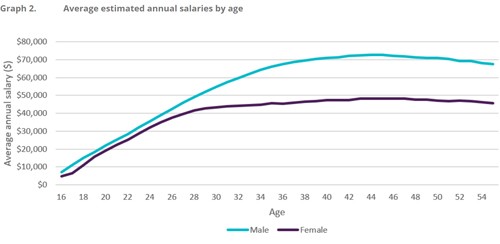

The research also demonstrates that women start out their careers with pay that is close to their male counterparts, only to see a gap emerge as women enter their 20s and 30s. The source of this divergence is not clear, but one likely cause is that women are more likely to leave work to take care of children or family members, missing out on years in the workforce when promotions and pay raises are most likely.

Investment research shows that men tend to invest more aggressively than women, but Rice Warner said this difference did not contribute significantly to the super gap.

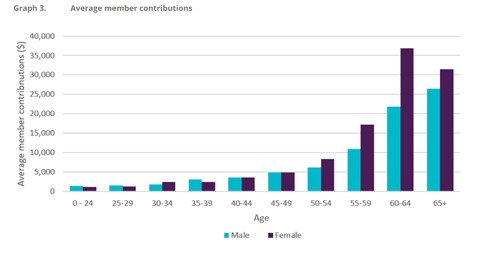

The positive news is that women are taking action to close the gap. They contribute more to super, especially as they approach retirement, which boosts their balances at a crucial stage.

Many women don’t earn enough to make extra contributions, however, and those who do likely can’t compensate enough for years of reduced earnings and super guarantee payments. The roots of the super pay gap are many — gender inequality, the challenges and costs of child care and super policy. Fixing the problem will require changes on all those fronts.

Written by Robin Bowerman

Head of Corporate Affairs at Vanguard.

21 May 2019

vanguardinvestments.com.au

More Articles

The evolution of the world’s languages

Check out the evolution of the world's most spoken languages from 2500 BC to...

Adequate retirement savings misjudged

Association of Superannuation Funds of Australia (ASFA) research has shown individuals across the country are...

Record SMSF growth driven by digital access

Record SMSF growth driven by AI and digital tools, but admin and compliance challenges...

The SBSCH will close from 1 July 2026

The ATO is warning employers not to use the small business super clearing house (SBSCH) for any further...

Rules apply to gifting in superannuation

Australia’s age pension gifting rules are again under scrutiny as advisers warn that retirees are...

Complications of maintaining two cost bases in Div 296

According to BT technical consultant Matt Manning, the Division 296 cost base reset requires SMSFs to maintain...

investment and economic outlook 2026

Our latest forecasts for investment returns and region-by-region economic outlook . Economic...

What the Payday Super changes mean for your retirement

Significant reforms to the Australian superannuation system are about to take effect and could help people...

Heathmont Financial Services Pty Ltd (ABN 68 106 250 104) trading as Heathmont Financial Services is a Corporate Authorised Representative (No. 262098) of Knox Wealth Management Pty Ltd (ABN 74 630 256 227), Australian Financial Services Licence Number (AFSL) 513763.

Julian McGoldrick is an Authorised Representative (No. 262098) of Knox Wealth Management Pty Ltd AFSL 513763.